In this article, we’re about to break down everything you need to know about the home loan rate drops – and more importantly, how you can pocket some serious savings! 💰

The Reserve Bank of India just gave us all an early gift by slashing the repo rate by a whopping 100 basis points (that’s 1% in plain English) from 6.5% to 5.5% in just six months. Think of the repo rate as the “master key” that unlocks lower interest rates across the banking system.

But here’s the million-rupee question: Will YOU actually benefit from these cuts? That depends on something called your loan’s “interest rate regime” – basically, which rulebook your bank follows to set your interest rate.

Don’t worry if this sounds like financial jargon soup. I’m here to translate everything into bite-sized, actionable insights that’ll help you make the smartest move for your wallet!

MCLR or RLLR: What’s Your Loan Speaking?

Let me paint you a picture. Your home loan’s interest rate is like a dance partner – it follows different music depending on when you started dancing (took the loan).

Got your loan between 2010-2016? You’re dancing to the “base rate” tune.

Loan taken from 2016-2019? You’re following the MCLR rhythm.

Borrowed after October 2019? Welcome to the RLLR party!

Here’s what’s fascinating: As of December 2024, about 61% of floating-rate loans are grooving to the repo rate (RLLR), while 36% are still moving to the slower MCLR beat. Only 3% are following other tunes.

Think of it this way – if interest rate changes were weather updates, RLLR loans get real-time alerts while MCLR loans rely on yesterday’s forecast!

The Tale of Two Rate Systems: MCLR vs RLLR

Let me explain these two systems using a simple analogy. Imagine you’re ordering food:

MCLR (Marginal Cost of Funds Based Lending Rate) is like ordering from a restaurant where the chef decides prices based on ingredient costs, kitchen expenses, and their mood. The menu gets updated maybe once or twice a year. Banks set this rate based on their internal costs – things like how much they pay for deposits, operating expenses, and market liquidity.

RLLR (Repo Linked Lending Rate) is like ordering from a food truck that updates prices based on today’s wholesale market rates. The menu changes quickly when costs change. Your rate = Current repo rate + Bank’s markup (spread).

The game-changer? Speed of transmission!

MCLR loans: Banks typically take 6-12 months to pass on rate changes. It’s like waiting for a slow-moving freight train.

RLLR loans: Banks must reset rates at least every three months. It’s like catching the express train – you reach your destination (savings) much faster!

Here’s how banks have actually adjusted rates in 2025:

- Repo rate cut: 100 basis points

- Average MCLR reduction: Much slower to reflect changes

- RLLR adjustment: Nearly immediate reflection

MCLR vs RLLR: The Complete Comparison

| Parameter | MCLR | RLLR |

|---|---|---|

| Benchmark | Banks decide internally | Repo rate (external) |

| Reset Period | 6–12 months typically | Every 3 months (quarterly) |

| Transparency | Moderate – depends on bank policies | High – directly linked to RBI rate |

| Speed of Transmission | Slower (like a diesel engine) | Faster (like an electric motor) |

| Rate Changes | Gradual, bank-dependent | Immediate with repo rate changes |

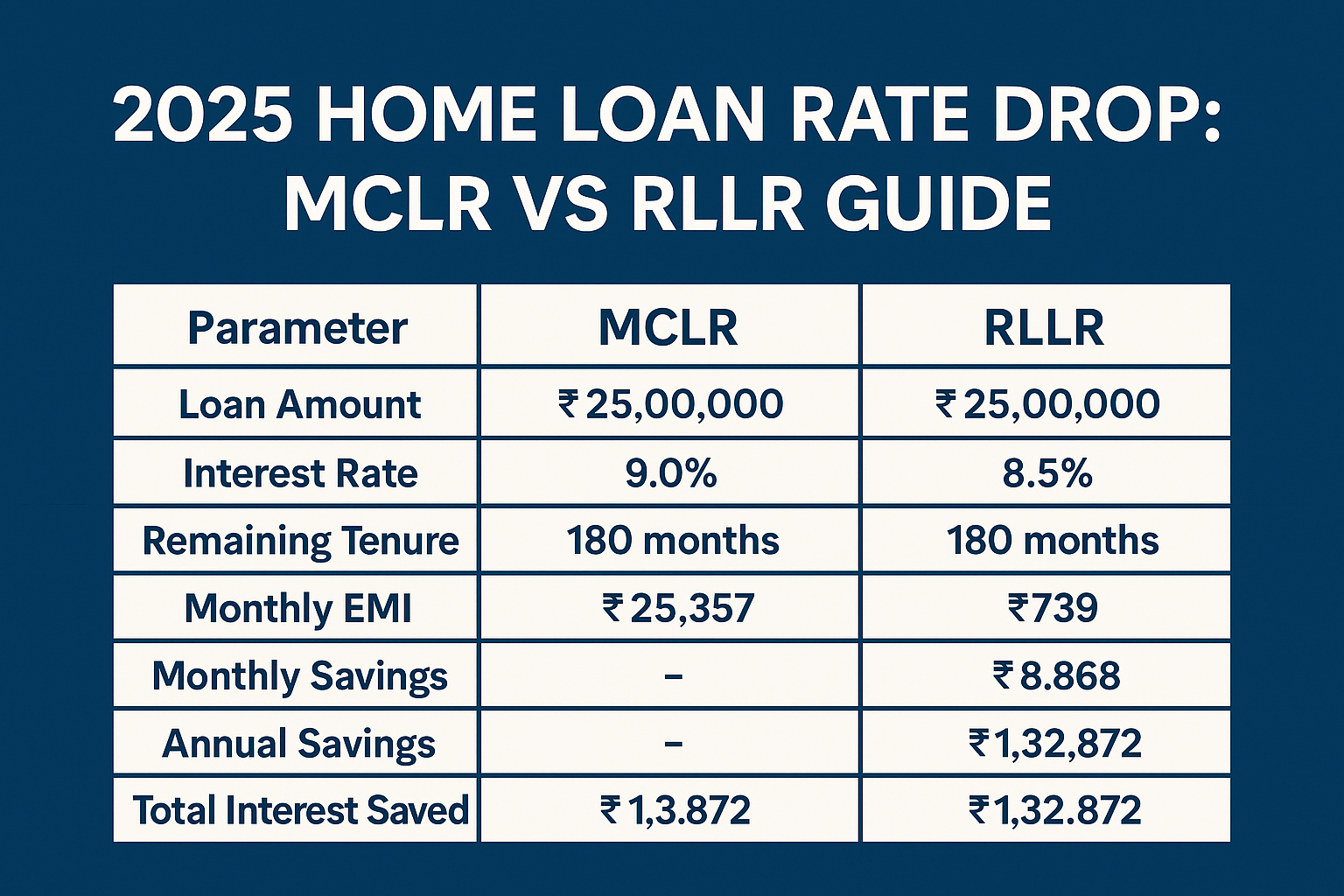

Show Me The Money: Real Savings Calculation

Let’s crunch some numbers with a real-world example that’ll make your calculator happy!

Your situation: ₹25 lakh outstanding loan, 15 years remaining

Current MCLR rate: 9% per annum

Available RLLR rate: 8.5% per annum

| Parameter | MCLR Loan | RLLR Loan |

|---|---|---|

| Loan Amount | ₹25,00,000 | ₹25,00,000 |

| Interest Rate | 9.0% | 8.5% |

| Remaining Tenure | 180 months | 180 months |

| Monthly EMI | ₹25,357 | ₹24,618 |

| Monthly Savings | – | ₹739 |

| Annual Savings | – | ₹8,868 |

| Total Interest Saved | – | ₹1,32,872 |

Can you imagine? Over ₹1.3 lakh in your pocket just by switching! That’s a nice vacation, kids’ education fund, or emergency buffer right there.

How to Switch: Your Action Plan

Ready to make the switch? Here’s your step-by-step playbook:

Step 1: Call your bank and say, “I want to switch to your repo-linked rate.”

Step 2: Ask about conversion fees. For example, HDFC Bank charges 0.25% of outstanding amount or ₹5,000 (whichever is lower), plus taxes.

Step 3: Do the math – will your savings outweigh the conversion cost?

Step 4: Submit your request and wait 7-15 days for processing.

Pro tip: Always calculate your break-even point. If the conversion fee is ₹10,000 and you save ₹739 monthly, you’ll recover the fee in about 14 months!

Reality Check: Not All Banks Are Playing Fair

Here’s something that might surprise you – not all banks are passing on the repo rate benefits equally! Our research shows some eye-opening differences:

| Bank Category | Rate Reduction (basis points) | Our Grade |

|---|---|---|

| Public Sector Banks | -70 bps | A+ (Excellent) |

| Housing Finance Companies | -40 bps | B+ (Good) |

| Private Banks | -15 bps | C- (Poor) |

| NBFCs | 0 bps | F (No transmission) |

| Small Finance Banks | 0 bps | F (No transmission) |

This is like going to different grocery stores during a wholesale price drop – some pass the savings to you, others keep the extra profit!

Your Pre-Switch Checklist

Before you jump ship, ask yourself these crucial questions:

✅ Does your bank offer repo-linked rates? They might call it EBLR, RLLR, or RBLR – the key is “repo rate” in the fine print.

✅ How much of the 100 bps repo cut has your bank passed on? If they’ve only passed 15 bps when the RBI cut 100 bps, that’s a red flag!

✅ What’s your total cost-benefit? Include conversion fees, potential savings, and time to break even.

✅ Should you switch banks entirely? Sometimes the grass really IS greener on the other side!

When to Consider a Complete Home Loan Transfer

If your current bank is being stingy with rate cuts, it might be time for a relationship status change from “It’s complicated” to “We’re done!”

Consider transferring your entire loan if:

- Your bank has poor transmission rates

- Another bank offers significantly better RLLR rates

- The total cost (including processing fees) still results in substantial savings

- You’re looking for better service anyway

The Bottom Line: Your Money, Your Choice

Look, the financial world can feel overwhelming, but this decision doesn’t have to be. The math is pretty clear – if you’re on an MCLR loan and your bank offers competitive RLLR rates with good transmission, switching is likely a smart move.

Remember: Every month you delay is money left on the table. That ₹739 monthly saving I calculated? Over a year, it could fund a family vacation, boost your emergency fund, or accelerate other financial goals.

Take Action Today

Don’t let this opportunity slip away like last year’s New Year’s resolutions! Here’s what to do right now:

- Check your loan documents – What regime are you currently on?

- Call your bank – What are their current RLLR rates?

- Use our calculator – Crunch your specific numbers

- Compare options – Sometimes switching banks beats switching regimes

- Get professional help – When in doubt, consult a qualified financial advisor

The repo rate cuts of 2025 have opened a window of opportunity. The question isn’t whether you CAN save money – it’s whether you WILL take action to save it.

Your future self will thank you for the extra cash in your bank account. After all, in the game of personal finance, every rupee saved is a rupee earned – and a step closer to financial freedom!

Disclaimer: This article provides educational information and personal opinions. Always consult with a qualified financial advisor before making loan decisions. Individual results may vary based on specific loan terms and bank policies.